Table of Contents

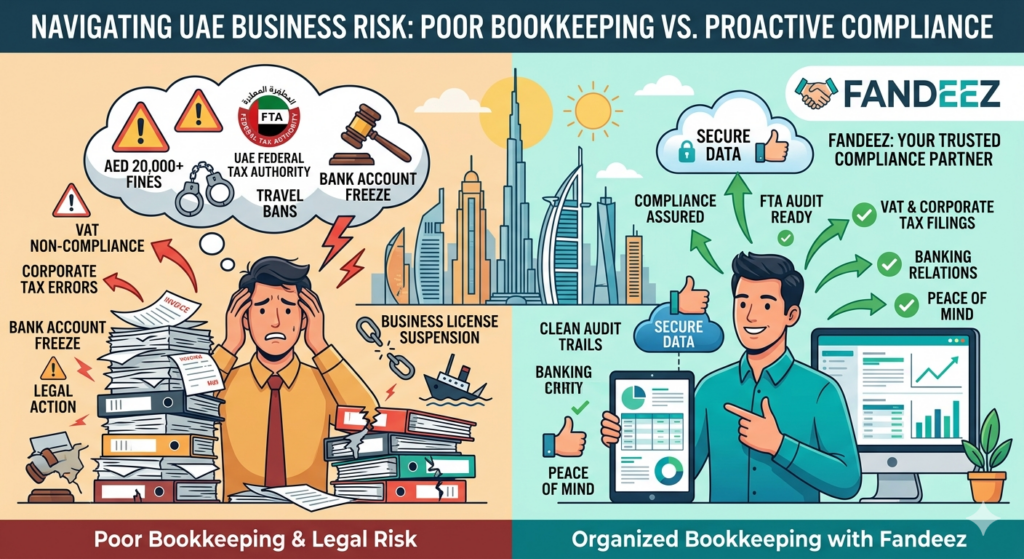

ToggleIn Dubai’s fast-moving business landscape, accurate financial records are not optional. They are a legal requirement. Yet many SMEs and startups underestimate how quickly disorganised books can lead to trouble. The poor bookkeeping legal risk UAE businesses face today is greater than ever, thanks to stricter enforcement by the Federal Tax Authority (FTA), mandatory corporate tax, and rigorous audit requirements.

A single missing invoice or unreconciled bank entry can snowball into heavy fines, damaged banking relationships, and even legal action. This article explains exactly what those risks are, how they apply to Dubai companies, and why working with a trusted partner like Fandeez is the smartest way to stay protected.

Why Accurate Bookkeeping Matters in Dubai & UAE

Dubai positions itself as a global business hub. With that status comes a commitment to financial transparency. The UAE government has built a compliance framework that demands every registered business maintain clear, auditable accounting records.

UAE bookkeeping compliance is not just about filing VAT on time. It requires:

- Recording every financial transaction accurately

- Retaining supporting documents for at least five years

- Ensuring records are available for FTA inspection at any time

Without this foundation, your business cannot prove its tax position, satisfy auditors, or even open a corporate bank account. In short, poor bookkeeping puts your entire operation at risk.

When Poor Bookkeeping Becomes a Legal Risk in the UAE

Many business owners assume that bookkeeping errors are harmless administrative oversights. In reality, the bookkeeping legal risks UAE authorities enforce are severe. The transition from messy records to legal trouble usually follows a clear path:

The FTA notices inconsistencies between your VAT returns and bank statements.

A formal audit request is issued.

You fail to produce complete, accurate records.

The case moves from administrative penalty to potential prosecution.

Once that happens, the poor bookkeeping legal risk UAE courts recognize includes willful negligence, tax evasion, and even fraud if records appear deliberately altered

VAT Compliance Risks From Poor Bookkeeping

VAT compliance bookkeeping UAE is a non-negotiable duty for any taxable business. Every VAT-registered company must file accurate returns every quarter or month. When your books are messy, errors become inevitable.

Common VAT-related risks include:

- Claiming input tax without valid tax invoices – Leads to recovery rejection and fines.

- Mismatched reporting – If your VAT return does not match your bank deposits, the FTA flags it automatically.

- Late adjustments – Missing credit notes or return entries distort your net VAT liability.

These mistakes trigger bookkeeping penalties UAE starts with AED 1,000 per missing invoice and escalates rapidly. The FTA now uses advanced data matching. They will find the error.

Corporate Tax Risks for UAE Businesses

The introduction of UAE Corporate Tax (9% on profits above AED 375,000) has raised the stakes dramatically. Corporate tax bookkeeping UAE requires businesses to calculate taxable income based on audited financial statements. If your records are unreliable, you cannot accurately determine your tax liability.

Specific risks include:

- Underreporting profits due to omitted sales – This is treated as tax evasion.

- Inflating expenses with unsupported entries – Deductions are disallowed, and penalties apply.

- Failing to maintain transfer pricing documentation – Related-party transactions must be clearly recorded.

Penalties for Corporate Tax non-compliance can reach 15% of the unpaid tax plus AED 20,000 or more for record-keeping violations. Unlike VAT, Corporate Tax errors also attract criminal liability for company directors.

Banking & Audit Problems Caused by Poor Financial Records

Beyond government penalties, poor bookkeeping destroys your credibility with banks and auditors. Dubai’s banking sector is highly regulated under anti-money laundering (AML) laws. Banks now require:

- Audited financial statements for loan approvals

- Clean transaction histories for account maintenance

- Clear source-of-funds documentation

If your poor accounting records UAE make it impossible to produce reliable statements, you face:

- Loan rejections and credit facility freezes

- Corporate bank account closures

- Blacklisting on AML databases

External auditors, when engaged, will issue a qualified opinion or deny an opinion altogether. That red flag scares off investors, partners, and even potential buyers for your business.

Common Bookkeeping Mistakes UAE Companies Make

Understanding the most frequent bookkeeping mistakes UAE businesses commit to helping you avoid them. Based on Fandeez’s work with hundreds of Dubai companies, these are the top offenders:

- Mixing personal and business expenses – This violates tax isolation rules and obscures true profitability.

- Not reconciling bank accounts monthly – Without reconciliation, errors go undetected for months or years.

- Losing or not retaining original invoices – The FTA requires physical or digital copies that are legible and complete.

- Ignoring accruals and prepayments – This distorts profit calculations for corporate tax.

- Using spreadsheets without audit trails – Manual sheets can be edited invisibly, making them FTA-unfriendly.

Even one of these errors elevates your UAE accounting compliance risk significantly.

Financial & Legal Consequences of Non-Compliance

So what are the actual bookkeeping penalties UAE businesses can expect? The FTA has published a clear penalty matrix. Here are the most relevant figures:

|

Violation |

Penalty |

|

Failure to keep proper accounting records |

AED 20,000 |

|

Each missing VAT invoice or document |

AED 1,000 (capped per assessment) |

|

Submitting false returns due to poor records |

AED 50,000+ |

|

Tax evasion via deliberate bookkeeping errors |

Up to 5x unpaid tax + imprisonment |

Beyond fines, the legal risks of poor bookkeeping include:

- Travel bans for directors

- Suspension or cancellation of trade licenses

- Criminal prosecution leading to jail time

In the UAE, ignorance is not a defense. The law holds business owners personally accountable for their company’s books.

How Dubai Businesses Can Stay Financially Compliant

Mitigating poor bookkeeping legal risk in the UAE requires a practical, proactive strategy. Here is what every Dubai business should do:

Adopt professional accounting software – cloud platforms like Zoho Books, QuickBooks, or Xero provide audit trails and automation.

Reconcile weekly or monthly – do not wait for year-end. Frequent reconciliation catches errors early.

Train staff on documentation – ensure every invoice, receipt, and contract is saved properly.

Conduct internal compliance reviews – check your books quarterly for red flags before the FTA does.

Outsource to experts – For most SMEs, hiring a full-time accountant is expensive. Partnering with a specialised firm ensures bookkeeping compliance in the UAE without the overhead.

The fifth point is critical. Compliance is a core competency that requires constant attention to changing laws.

Why Businesses Choose Fandeez in Dubai

This is where Fandeez makes the difference. Based in Dubai, we are a dedicated accounting, tax, and compliance firm that helps businesses eliminate compliance risk. We do not just record transactions; we build systems that keep you audit-ready at all times.

When you work with Fandeez, you get:

- End-to-end bookkeeping – Daily transaction recording, bank reconciliation, and ledger management.

- VAT and Corporate Tax readiness – Your books are structured for immediate, accurate filing.

- Penalty protection – We flag issues before they become fines.

- Audit support – If the FTA knocks, we provide the trail and representation.

- Tailored for Dubai businesses – We understand free zone, mainland, and offshore requirements.

Our clients range from startups to established SMEs. They choose Fandeez because we replace fear with confidence. No surprises. No last-minute scrambling. Just clean, compliant books.

Conclusion

The era of casual bookkeeping in the UAE is over. With the FTA’s digital cross-matching, mandatory corporate tax, and stricter banking AML rules, the poor bookkeeping legal risk UAE businesses face is now a board-level concern. From AED 20,000 fines to travel bans and imprisonment, the consequences are real.

But the solution is straightforward: maintain accurate, audit-ready records. And if that feels overwhelming, get expert help.

Don’t wait for a penalty notice. Let Fandeez protect your business with professional, proactive bookkeeping compliance. Contact us today for a free initial consultation and compliance health check